What Are Average Estate Sale Proceeds?

Discover the average estate sale proceeds and the key factors that determine your final profit. Learn how to maximize your earnings from any estate liquidation.

When you're planning an estate sale, the first question on everyone's mind is always the same: "How much money can I actually make?" It's the bottom line, and knowing what to expect is crucial.

Based on industry-wide data, the average estate sale typically grosses between $18,000 and $20,000. Think of this as a solid starting point—a benchmark for what a sale of a home's complete contents might bring in.

Understanding the Financial Snapshot of a Sale

It helps to think about your sale's earnings like a paycheck. The gross revenue is that big number at the top—the total amount of money the sale pulls in before anyone takes a cut. It's the sum of every item sold, from the antique armoire to the last teaspoon.

But just like your paycheck has deductions, your final take-home profit comes after the estate sale company's commission and any other fees are subtracted. Getting clear on this gross vs. net distinction from the start is the key to setting realistic financial goals.

From Gross Revenue to Your Net Profit

So, how does that top-line number translate into cash in your pocket? It's a pretty simple path.

After a typical professional company takes its commission, which usually runs between 35% and 40%, sellers can expect to net around $10,800 to $13,000 from an average sale. Data from sources like EstateSales.net consistently back this up. This is exactly why it’s so important to understand a company's commission structure before you sign a contract.

To make it even clearer, here’s a quick breakdown of how the numbers work out.

Estimated Estate Sale Proceeds at a Glance

This table shows how a typical gross revenue from an estate sale translates into the net proceeds you, the seller, will receive after commissions are paid.

| Metric | Low-End Estimate | High-End Estimate |

|---|---|---|

| Gross Sale Revenue | $18,000 | $20,000 |

| Commission Rate | 40% | 35% |

| Net Proceeds to Seller | $10,800 | $13,000 |

As you can see, the commission rate has a direct and significant impact on your final payout.

Why Averages Are Just the Beginning

It’s really important to treat that $18,000 to $20,000 figure as a baseline, not a guarantee. Every single home is different, and your final earnings will swing based on a whole host of factors we're about to dig into.

The single biggest driver of value is, without a doubt, the contents of the home. A house filled with everyday furniture and basic housewares will fetch a very different price than one that holds fine art, rare collections, or high-end designer pieces.

Ultimately, knowing the average gives you a valuable frame of reference. It helps you grasp the potential scale of your sale and prepares you to look closer at what really moves the needle—from the quality of your items to the skill of the company you hire.

How Estate Sale Commissions and Fees Work

To really get a handle on your financial expectations, you first need to understand how an estate sale company gets paid. The industry standard is a commission-based model. It’s a lot like hiring a real estate agent to sell your house; you’re paying a professional for their time, expertise, and connections to get the best possible result.

That commission isn't just a simple fee for running the event. It’s a comprehensive charge covering all the behind-the-scenes work that turns a home full of personal belongings into a successful, pop-up retail shop. Since this percentage directly affects your average estate sale proceeds, it’s crucial to know what you're paying for.

What Does the Commission Typically Include?

When you sign with a full-service estate sale company, their commission rate—which usually lands somewhere between 35% and 50%—is designed to cover a whole host of services. The goal is to make the entire process hands-off for you while generating the most revenue possible from the sale.

Think of the commission as an all-inclusive package. Generally, it covers:

- Sorting and Organizing: The physically demanding job of going through every single room, closet, and cabinet to sort items for the sale.

- Item Research and Pricing: This is a big one. It involves appraising thousands of individual items—from antique furniture and collectibles down to everyday kitchen gadgets—to hit that sweet spot between a competitive price and a profitable one.

- Staging and Merchandising: Good presentation is key. They'll transform the home into a shoppable space, cleaning and arranging everything to create an appealing environment for buyers.

- Professional Advertising and Marketing: Getting the word out is critical. This includes promoting the sale on specialized listing sites, social media, and through their own email lists of dedicated local shoppers.

- Staffing the Sale: You need people on the ground. The fee covers the team needed to manage the crowds, answer questions, and handle checkout during the one-to-three-day event.

- Payment Processing: Securely handling all the money, whether it’s cash or credit card payments.

These core services are the engine that powers a profitable sale, and their cost is baked right into the company's percentage. If you want to get into the nitty-gritty of these rates, you can learn more about the average estate sale commission and what influences it.

Understanding Additional Fees and Minimums

While the commission fee is designed to be comprehensive, some situations can lead to extra charges. These are almost always for specialized tasks or unusually demanding work that falls outside the scope of a typical sale.

Important Note: Always get clarity on potential extra costs before you sign a contract. Any reputable company will be completely transparent about what their commission covers and what it doesn't.

Some common extra costs you might run into include:

- Specialist Appraisals: If you have high-value items like fine art, significant jewelry collections, or rare antiques, they may need to bring in a certified third-party appraiser.

- Major Trash Haul-Away: Sometimes a property has a large amount of unsaleable clutter or trash that needs to be removed before the team can even begin setting up.

- Heavy Item Moving: For exceptionally large or heavy pieces, like a concert grand piano or a massive safe, professional movers might be required.

Finally, it’s important to know that many companies have a company minimum. This is a policy where they will only take on sales that are projected to gross a certain amount, often $10,000 or more. This ensures the sale will be profitable enough to cover their substantial operating costs while still leaving you with a meaningful check at the end.

Key Factors That Determine Your Final Profit

So, why does one estate sale bring in a modest $5,000 while another down the street nets over $50,000? It's never just one thing. The final number is always a mix of specific variables all working together.

Think of it like baking a cake. You need the right ingredients (your items), the right oven temperature (the market), and the right recipe (the sale strategy). If any one of those is off, the result just won't rise to its full potential. Let's break down the three key areas that really move the needle on your bottom line.

The Quality and Type of Items

Without a doubt, the single biggest factor dictating your sale's success is the quality and desirability of the items in the home. Not all belongings are created equal in the eyes of buyers. A house full of standard, used furniture and everyday housewares will generate a certain level of income, but it's the standout categories that can really boost the total.

Here’s a look at what can dramatically affect the outcome:

- High-Demand Collections: Specialized collections—like vintage vinyl records, rare books, or well-maintained antique tools—attract passionate buyers willing to pay premium prices.

- Fine Art and Jewelry: Original paintings, sculptures, and high-quality gold or silver jewelry are major revenue drivers. Their value often requires an expert eye to maximize returns.

- Designer and Brand-Name Goods: Authentic designer furniture (think mid-century modern), high-end fashion, and luxury handbags have a very strong resale market and draw serious bidders.

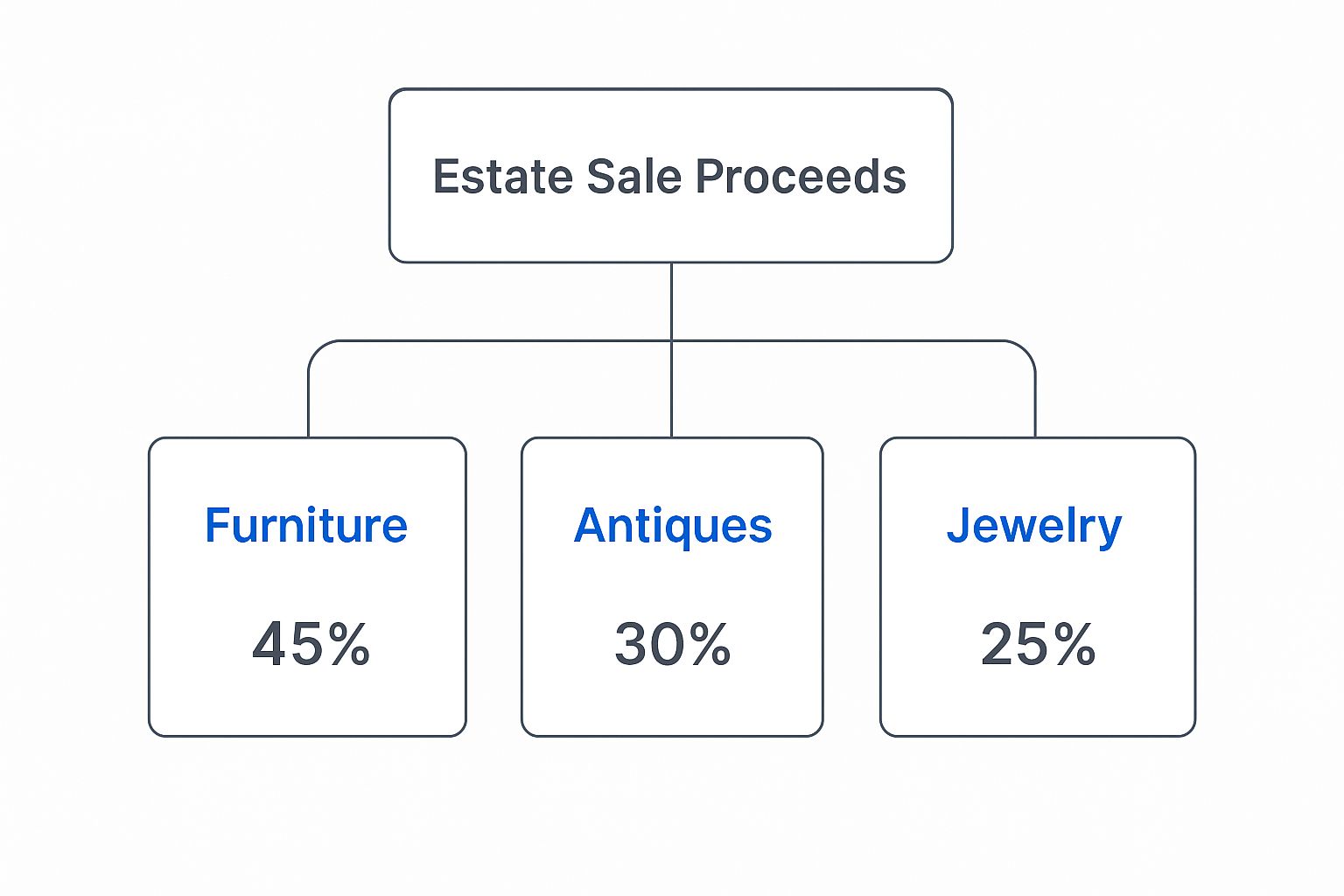

This image shows where the money typically comes from in a higher-value estate sale.

As you can see, substantial items like furniture, antiques, and jewelry usually account for the biggest slice of the pie.

Your Market and Location

Where you hold the sale is almost as important as what you're selling. The local market—buyer demand, regional tastes, and even the local economy—plays a huge role in your final numbers.

Imagine trying to sell a collection of sought-after mid-century modern furniture. In a large, design-savvy city like Los Angeles or Austin, you'd likely see a bidding war. In a small, rural town with different tastes, those same pieces might struggle to sell for a fraction of the price.

Your location directly impacts the size and enthusiasm of your buyer pool. A sale in a packed, affluent suburb will naturally attract more foot traffic than one in a remote, hard-to-reach area. This is where a professional company’s local expertise really pays off.

The Strategy of Your Sale Company

Finally, the skill and strategy of the estate sale company you hire can absolutely make or break your event. A great company does way more than just put price tags on things; they are marketers, merchandisers, and project managers all rolled into one.

Their network of loyal buyers, their advertising reach, and their ability to create a "buzz" around your sale directly impact the final tally.

Data from the 2023 Estate Sale Industry Survey highlights just how varied sales can be. While most sales (70.57%) generate under $20,000, the sheer volume of items is a huge factor—the largest group of sales (23.17%) contains between 1,000 and 1,999 items. These figures prove that both the value and volume of your inventory are critical.

A top-tier company knows how to price items competitively, stage the home to feel more like a boutique, and market the event to thousands of potential customers. It’s their job to make sure every valuable item finds the right buyer for the right price.

The Bigger Picture of Estate Liquidation

It’s easy to think of an estate sale as just a one-off event, but it's really a single transaction in a huge, established industry. Understanding this market context is the key to figuring out what drives your average estate sale proceeds and why choosing the right partner is so important.

Think of it this way: you’re not just holding a giant garage sale. You're stepping into a marketplace shaped by major economic and demographic forces. These trends influence everything from what buyers are looking for to what your items are worth.

A Growing and Professionalizing Industry

The estate liquidation market has moved far beyond a simple niche service. Trends like an aging population and constant shifts in real estate have cranked up the demand for professional help. Because of this, the industry has evolved from basic tag sales to sophisticated, full-service operations.

The Estate Liquidation Services industry is a serious business, with revenues expected to hit $230.3 million in 2024. This growth is fueled by a steady stream of estates that need to be settled efficiently and professionally.

This boom has pushed companies to offer much more than a three-day sale. Many now provide a complete package to manage the entire process—from sorting and appraising to the final clean-out. To see how these services are bundled, you can check out our guide on what estate sale fees typically cover.

Why This Market Context Matters to You

So, what does all this industry talk mean for you? It highlights the massive value a strategic partner brings to the table. A modern, full-service company isn’t just trying to get quick cash for your stuff; they’re focused on maximizing the value of the entire estate. Their job is to navigate the market's complexities for you.

This professional approach is a direct answer to the growing need for reliable and transparent liquidation. Research shows that things like fluctuating mortgage rates and more senior households are feeding this demand.

When you see your sale as part of this bigger picture, you can make a smarter decision. It helps ensure you partner with someone who can deliver the best possible financial outcome for the whole estate.

Actionable Strategies to Maximize Your Earnings

While industry averages give you a ballpark figure, your final profit isn't set in stone. You actually have a surprising amount of influence over the final outcome.

Think of it less like a lottery and more like a partnership. A few smart moves on your end can easily add thousands to your final check, turning an "average" sale into an exceptional one. These aren't just theories; they're practical steps that work.

The Golden Rule: Don't Throw Anything Away

If you remember only one thing, make it this. It’s the single most important rule when preparing for an estate sale. That pile of old papers, a tangled box of costume jewelry, or a dusty stack of records could hold some of the most valuable items in the house.

So many well-meaning families try to "clean up" before calling in a professional, and in the process, they accidentally toss out the hidden gems. An experienced estate sale pro has a trained eye for spotting value where most people would see junk. Let them be the ones to sort the treasure from the trash—it’s a huge part of what you’re paying for.

Key Insight: We’ve seen incredible finds pulled from the most unlikely places—forgotten tool sheds, attics crammed with old letters and photos, and closets filled with vintage clothing. To give your sale its best shot, leave everything for professional review.

Vet Your Estate Sale Company Thoroughly

Choosing the right company is about so much more than finding the lowest commission rate. In fact, a cheap company that runs a poorly marketed, disorganized sale will net you far less than a top-tier crew with a slightly higher fee.

When you’re interviewing companies, you need to dig deep into their actual process.

- Marketing Strategy: Don't just take their word for it; ask to see examples of their advertising. How big is their email list and social media following? A company with over 10,000 engaged followers has a massive head start.

- Experience and Specialization: Do they have a track record with the specific kind of items in the estate? If you have a lot of fine art, military memorabilia, or antique tools, you need someone who knows that market inside and out.

- Online Presence: Check out their past sales on sites like EstateSales.net. Are the photos sharp and professional? Are the descriptions detailed and enticing?

Doing this homework upfront pays off big time. It ensures you partner with a team that can attract a huge, motivated crowd of buyers who are ready to spend.

Prepare the Home and Your Documentation

Once you’ve hired your company, your job is to help them succeed. It starts by creating an inviting shopping environment. A clean, bright, and uncluttered home encourages buyers to stick around longer and look more closely. Simple actions like opening the blinds, cleaning the windows, and making sure the house smells fresh can make a world of difference.

Next, gather up any paperwork you have for the more valuable items. This could include:

- Original receipts

- Certificates of authenticity

- Previous appraisals

Handing this documentation over to the sale manager helps them price items accurately and gives buyers the confidence to pay top dollar. This groundwork directly supports their efforts and can seriously boost the value of your most important pieces. For a closer look at this crucial step, you can find great advice on how to price estate sale items and understand what paperwork truly matters.

Common Questions We Hear About Estate Sale Proceeds

Even after you've hashed out the major details, a few specific questions always pop up as the sale gets closer. Let's be honest, these are the make-or-break details that determine how smoothly everything goes.

Here are the straight answers to the questions we hear most often.

Are Estate Sale Proceeds Taxable?

This is a big one, and thankfully, the answer is usually straightforward. For the vast majority of families, no, the proceeds are not taxable income.

Why? Because you're typically selling everyday personal belongings for far less than what you (or your loved one) originally paid for them. Since there's no profit, there's nothing for the IRS to tax.

The only time this changes is if you sell a high-value asset—think fine art, a rare coin collection, or a significant antique—for more than its original purchase price. That gain could trigger a capital gains tax. Every family's situation is different, so it's always a smart move to have a quick chat with a tax professional.

What Happens to Items That Don't Sell?

It's the reality of every sale: not everything will find a new home. No estate sale ever sells 100% of the inventory. So, what happens to the leftovers? Your contract with the estate sale company will spell this out clearly.

You'll generally see a few standard options:

- Charitable Donation: This is the most popular route. The company handles all the logistics of getting the remaining items to a local charity, and you get a donation receipt for a potential tax write-off.

- Company Buy-Out: Some companies offer to buy everything that's left for a flat, pre-negotiated price. It's a clean, fast way to wrap things up and empty the house.

- Final Clean-Out: If you just want it all gone, you can opt for a clean-out service to haul everything away. This usually comes with an extra fee but leaves the property completely empty.

It's so important to decide on this before the sale begins. Having a clear plan for the unsold goods saves a ton of last-minute stress and ensures the house is broom-clean and ready for whatever comes next.

How Soon Do I Get Paid After the Sale?

Once the last shopper has paid and the doors are closed, you're on the home stretch. The timeline for getting your money and a final sales report is another key detail that should be in your contract.

Most reputable companies settle up within 7 to 21 days after the sale ends. This gives them enough time to make sure all credit card payments have cleared (which can take a few business days) and to put together your detailed financial statement.

This report will break down the gross sales total, subtract the company's commission and any other fees you agreed to, and show your final net proceeds.

More guides in Estate Sale Basics

July 26, 2026

Stamp Collection Valuation: A Practical Step-by-Step Guide

Stamp collection valuation made simple. Learn how to identify, grade, price, and sell your stamps with confidence for estate sales or consignment.

Read guideJuly 23, 2026

Estate Sales Brick NJ: Your 2026 Guide to Success

Planning your estate sales brick nj? Our guide covers permits, pricing, marketing, & running a safe sale with DIYAuctions.

Read guideJuly 19, 2026

How to Prevent No Shows at Your Estate Sale

Learn how to prevent no shows for your estate sale pickup. Our guide offers actionable policies, reminder templates, and scheduling tips for a smooth event.

Read guideGet the estate sale pricing guide

Enter your email for pricing ranges, planning notes, and a clearer path to launch.